{COMPANY_NAME}

(877) 420-2341

INJURED SPOUSE CLAIM &

INNOCENT SPOUSE RULE

Do you believe you might qualify under the injured spouse or innocent spouse rule? These are precise definitions under IRS rules and can be difficult to document. Our US Tax Relief attorneys have extensive experience in this area, and can help you navigate this part of the tax code. First let's define the rules so you can get a better idea of whether you will qualify.

If you’re married, there are two status options you can choose between when filing your federal tax return: Married Filing Separately and Married Filing Jointly. When spouses file their taxes separately, they each complete their own Form 1040. The IRS discourages this by offering hefty tax advantages to those who file jointly. If you file separately, you could disqualify or limit your use of potentially valuable tax breaks, including, but not limited to

- The Earned Income credit

- The child and dependent credit

- The American Opportunity credit

- The Lifetime Learning credit

- Tax-free exclusion of Social Security benefits

- The adoption credit

- The credit for the elderly and disabled

- The deduction of net capital losses

- The deduction for college tuition expenses

- Tax-free exclusion of U.S. bond interest

- The student loan interest deductions

- Traditional IRA deductions

- Roth IRA contributions

With so many tax deductions to take advantage of, it’s easy to see why so many couples choose to file jointly.

However, there’s one significant disadvantage to a Married Filing Jointly status, and it’s called “joint and several liability”. Joint and several liability is when multiple parties can be held liable for the same event or act and be responsible for all restitution required. As it relates to taxes, both taxpayers in a Married Filing Jointly return are jointly and severally liable for the tax and any additions to tax, interest, or penalties that arise from the joint return even if they later divorce.

Both spouses are generally held responsible for all the tax due even if one spouse earned all the income or claimed improper deductions or credits. By filing separately, you gain separation of tax liability from your spouse and are only responsible for the payment of taxes for your own return. If you’ve previously completed a Married Filing Jointly return, and now find yourself in trouble paying for your spouse’s error, there are a few instances in which the IRS offers liability relief.

Both spouses are generally held responsible for all the tax due even if one spouse earned all the income or claimed improper deductions or credits. By filing separately, you gain separation of tax liability from your spouse and are only responsible for the payment of taxes for your own return. If you’ve previously completed a Married Filing Jointly return, and now find yourself in trouble paying for your spouse’s error, there are a few instances in which the IRS offers liability relief.

SPEAK WITH ONE OF OUR TAX PROFESSIONALS TODAY

FREE CONSULTATION

{"name":"Contact Button b","action_type":"1","optin_action_type":"5","form_redirect_type":"1","form_redirect_funnel_url":"5ecea1dde7bd0","form_redirect_custom_url":"","order_form_settings":{"containers":[{"id":"personal-info-wrapper","visible":true,"label":{"id":"of-personal-title","visible":true},"fields":[{"id":"of-full-name","setting":false,"placeholder":"Full Name"},{"id":"of-field-email","setting":false,"placeholder":"Email Address"},{"id":"of-phone-number","setting":true,"visible":false,"require":true,"placeholder":"Enter Your Mobile Phone","additional":{"sms_permission":0}},{"id":"of-gdpr-optin-approval","label":"I Accept To Receive Additional Info","placeholder":"","icon":"fa-mobile","required":0,"visible":0,"system":1,"additional":{"gdpr_optin_approval":"1"}}]},{"id":"shipping-information-wrapper","visible":false,"label":{"id":"of-shipping-title","visible":true},"fields":[{"id":"of-shipping-address","setting":false,"placeholder":"Address"},{"id":"of-shipping-city","setting":false,"placeholder":"City"},{"id":"of-shipping-state","setting":false,"placeholder":"State"},{"id":"of-shipping-zipcode","setting":false,"placeholder":"Postal Code"}]},{"id":"credit-card-wrapper","visible":true,"label":{"id":"of-ccard-title","visible":true},"fields":[{"id":"of-ccard-number","setting":false,"placeholder":"Credit Card Number"},{"id":"of-ccard-cvc","setting":false,"placeholder":"CVC"}]},{"id":"profit-bump-wrapper","visible":true,"otoBgColor":"rgba(219,229,239,1)","otoBorderColor":"rgba(38,71,102,1)","otoTitleBgColor":"rgba(45,78,108,1)","otoArrowsColor":"rgba(255,177,58,1)","fields":[]},{"id":"order-summary-wrapper","visible":true,"orderDynamicBgColor":"rgba(242,242,242,1)","orderDynamicTexColor":"rgba(51,51,51,1)","fields":[]}]},"optin_type":{"showLabels":0,"fields":[{"name":"first_name","label":"Full Name","placeholder":"Enter Your Full Name","icon":"fa-user","required":1,"visible":1,"system":1,"additional":{}},{"name":"last_name","label":"Full Name","placeholder":"Enter Your Full Name","icon":"fa-user","required":1,"visible":1,"system":1,"additional":{}},{"name":"email","label":"Email","placeholder":"Enter Your Email","icon":"fa-envelope","required":1,"visible":1,"system":1,"additional":{}},{"name":"mobile_phone","label":"Mobile Phone","placeholder":"Enter Your Mobile Phone","icon":"fa-mobile","required":0,"visible":0,"system":1,"additional":{"sms_permission":0}},{"name":"fields_labels","label":"","placeholder":"","icon":"","required":0,"visible":1,"system":1,"additional":{}},{"name":"captcha","label":"Captcha","placeholder":"","icon":"","required":0,"visible":0,"system":1,"additional":{}},{"name":"gdpr_optin_approval","label":"SSBBY2NlcHQgVG8gUmVjZWl2ZSBBZGRpdGlvbmFsIEluZm8=","placeholder":"","icon":"fa-mobile","required":0,"visible":1,"system":1,"additional":{"gdpr_optin_approval":"1","sms_permission":0}}],"customFields":[],"sortedFields":[{"name":"first_name","label":"Full Name","placeholder":"Enter Your Full Name","icon":"fa-user","required":1,"visible":1,"system":1,"additional":{}},{"name":"first_name","label":"Full Name","placeholder":"Enter Your Full Name","icon":"fa-user","required":1,"visible":1,"system":1,"additional":{}},{"name":"last_name","label":"Full Name","placeholder":"Enter Your Full Name","icon":"fa-user","required":1,"visible":1,"system":1,"additional":{}},{"name":"email","label":"Email","placeholder":"Enter Your Email","icon":"fa-envelope","required":1,"visible":1,"system":1,"additional":{}},{"name":"mobile_phone","label":"Mobile Phone","placeholder":"Enter Your Mobile Phone","icon":"fa-mobile","required":0,"visible":0,"system":1,"additional":{"sms_permission":0}},{"name":"captcha","label":"Captcha","placeholder":"","icon":"","required":0,"visible":0,"system":1,"additional":{}}],"design":{"form_background_color":"rgb(245, 245, 245)","field_stroke":{"size":"1","color":"rgb(220, 220, 220)"},"field_icons":1,"button_color":"rgb(255, 158, 0)","button_stroke":{"size":"0","color":"rgba(255, 255, 255, 0.2)"},"button_box_shadow_color":"rgb(213, 139, 18) 0px 2px 0px 0px","field_size":"small","label_size":"16","label_color":"rgb(3, 3, 3)","input_color":"rgb(52, 152, 219)","control_text_color":"rgb(3, 3, 3)","control_text_size":"15"},"mappedFields":[]},"redirect_type":{"url":"https://112785.funnelpages.com/contact-us","target":1},"next_step":{"value":"5ecea1dde7bd0"},"click_to_email":{"value":""},"click_to_call":{"value":""},"jump_to_block":{},"content":{"header_text":"PHNwYW4gc3R5bGU9ImZvbnQtc2l6ZToyNHB4OyBmb250LWZhbWlseTonb3BlbiBzYW5zJzsiPjxzcGFuIHN0eWxlPSJsaW5lLWhlaWdodDoxLjRlbTsiPldlIEFyZSBFeGNpdGVkITwvc3Bhbj48L3NwYW4+","content_text":"PHNwYW4gc3R5bGU9ImZvbnQtc2l6ZTo0OHB4OyBmb250LWZhbWlseTonb3BlbiBzYW5zJzsiPjxzcGFuIHN0eWxlPSJsaW5lLWhlaWdodDowLjllbTsiPjxzdHJvbmc+UExFQVNFIEZJTEwgT1VUIFlPVVIgSU5GTyAgQkVMT1cgVE8gU1VCU0NSSUJFPC9zdHJvbmc+PC9zcGFuPjwvc3Bhbj4=","button_text":"dW5kZWZpbmVk","spam_text":"PHNwYW4gc3R5bGU9ImxpbmUtaGVpZ2h0OjEuMmVtOyI+V2UgaGF0ZSBTUEFNIGFuZCBwcm9taXNlIHRvIGtlZXAgeW91ciBlbWFpbCBhZGRyZXNzIHNhZmU8L3NwYW4+","sms_text":"UmVjZWl2ZSBTTVMgVGV4dCBVcGRhdGVzIC0gPHNwYW4+b3B0aW9uYWw8L3NwYW4+","sms_text2":"SSBBY2NlcHQgVG8gUmVjZWl2ZSBBZGRpdGlvbmFsIEluZm8="},"email_confirmation":{"enable":1,"subject":"V2UgQXJlIEV4Y2l0ZWQhIFlvdXIgSW4h","message":""},"integrations":{"name":"Form Optin Conversion","tag_id":""},"automation_enable":0,"thank_you":{"type":"popup","redirect_url":"","popup_options":{"background_color":"#ffffff","headline_visible":1,"icon_visible":1,"icon_url":"//my.funnelpages.com/assets-pb/images/thankyou-popup-icon.png","subheadline_visible":1,"button_visible":1,"button_color":"#ffa800","headline_text":"PHNwYW4gc3R5bGU9ImxpbmUtaGVpZ2h0OjEuNGVtOyI+VGhhbmsgWW91IEZvciBDb250YWN0aW5nIFVzPC9zcGFuPg==","subeadline_text":"PHNwYW4gc3R5bGU9ImxpbmUtaGVpZ2h0OjEuNGVtOyI+UGxlYXNlIENoZWNrIFlvdXIgRW1haWw8YnIgLz5XZSBXaWxsIEJlIEZvbGxvd2luZyBVcCBTaG9ydGx5PC9zcGFuPg==","button_text":"Q2xvc2U="}}}

Differences between Injured Spouse vs Innocent Spouse

Innocent spouse relief might be offered when your current or former spouse failed to report income, reported income improperly, or claimed improper deductions and credits. To qualify as an innocent spouse, the IRS says you must meet all the following requirements:

- You filed a joint return that had an understatement of tax (deficiency) that’s solely attributed to your spouse’s erroneous item. Erroneous items include the income received by your spouse but omitted from the return, as well as incorrectly reported deductions, credits, and property basis.

- You establish at the time you signed the return that you didn’t know, and had no reason to know, that there was an understatement of tax.

- Taking into account all the facts and circumstances, it would be unfair to hold you liable for the understatement of tax.

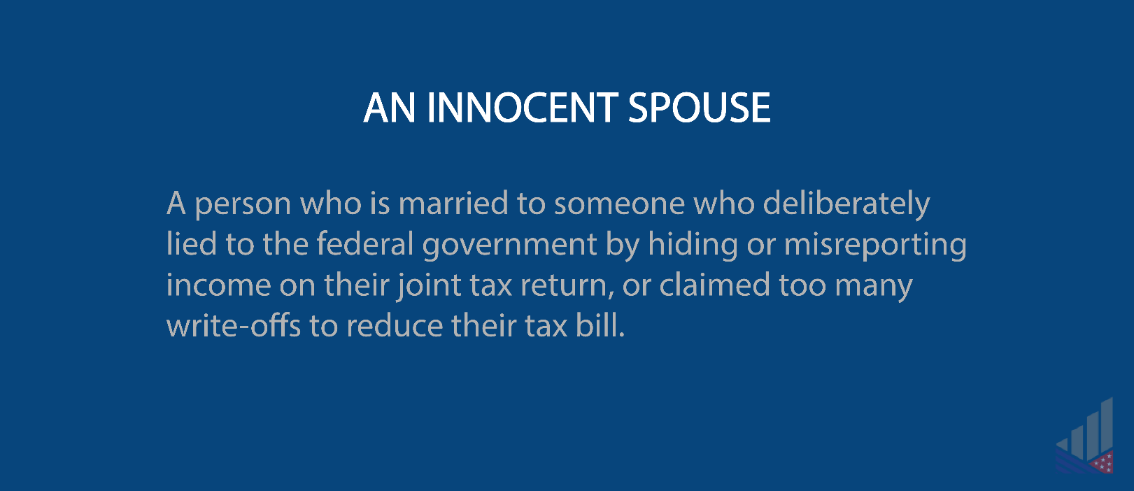

In short, an innocent spouse is married to someone who, on their joint tax return, deliberately lied to the federal government by hiding or misreporting income or claimed too many write-offs to lower their tax bill. If you had no idea about this understatement at the time you signed your tax return form, the government doesn’t think you should also be held accountable for the penalty and might qualify you for innocent spouse relief from joint and several liability.

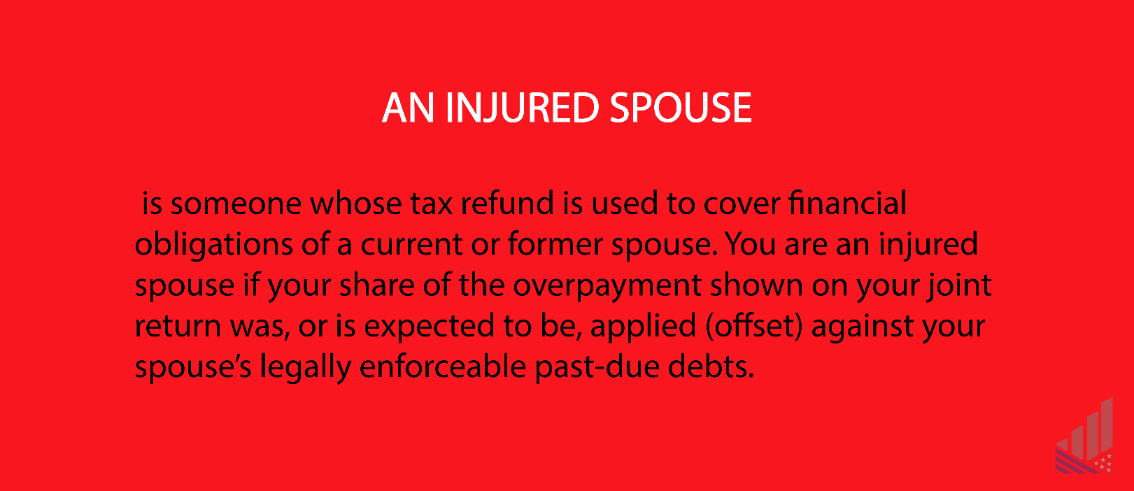

To be considered an injured spouse, you must have paid federal income tax or claimed a refundable tax credit, such as the Earned Income Credit in Notice 797 or Additional Child Tax Credit on the joint return, and not be legally obligated to pay the debt of the spouse.

To be considered an injured spouse, you must have paid federal income tax or claimed a refundable tax credit, such as the Earned Income Credit in Notice 797 or Additional Child Tax Credit on the joint return, and not be legally obligated to pay the debt of the spouse.

Rules for Injured Spouse vs Innocent Spous

If you file a joint return with your spouse, the IRS will not automatically distinguish between you and your partner when collecting tax dollars from either of you, even if your spouse’s debt existed well before the marriage. The IRS has the legal right to offset some or all of a refund to apply to unpaid financial responsibilities such as:

- Federal taxes

- State income taxes

- State unemployment compensation debts

- Child or spousal support payments

- Federal nontax debt, such as defaulted student loans

When the IRS applies a person’s refund to past debt, they will mail a formal Notice of Offset to the taxpayer’s address. At this time, the taxpayer whose refund was seized or offset can file an injured spouse claim. The IRS has up to 14 weeks to respond, so your refund may be delayed for quite a while. Special rules might apply to injured spouse claim in community property states (Louisiana, Arizona, California, Texas, Washington, Idaho, Nevada, New Mexico, and Wisconsin).

Community property states follow the rule that all assets acquired during the marriage are considered “community property”. For more information about the factors used to determine whether you are subject to community property laws, see IRS Publication 555, Community Property.

Community property states follow the rule that all assets acquired during the marriage are considered “community property”. For more information about the factors used to determine whether you are subject to community property laws, see IRS Publication 555, Community Property.

SPEAK WITH ONE OF OUR TAX PROFESSIONALS TODAY

FREE CONSULTATION

{"name":"Contact Button","action_type":"1","optin_action_type":"5","form_redirect_type":"1","form_redirect_funnel_url":"5ecea1dde7bd0","form_redirect_custom_url":"","order_form_settings":{"containers":[{"id":"personal-info-wrapper","visible":true,"label":{"id":"of-personal-title","visible":true},"fields":[{"id":"of-full-name","setting":false,"placeholder":"Full Name"},{"id":"of-field-email","setting":false,"placeholder":"Email Address"},{"id":"of-phone-number","setting":true,"visible":false,"require":true,"placeholder":"Enter Your Mobile Phone","additional":{"sms_permission":0}},{"id":"of-gdpr-optin-approval","label":"I Accept To Receive Additional Info","placeholder":"","icon":"fa-mobile","required":0,"visible":0,"system":1,"additional":{"gdpr_optin_approval":"1"}}]},{"id":"shipping-information-wrapper","visible":false,"label":{"id":"of-shipping-title","visible":true},"fields":[{"id":"of-shipping-address","setting":false,"placeholder":"Address"},{"id":"of-shipping-city","setting":false,"placeholder":"City"},{"id":"of-shipping-state","setting":false,"placeholder":"State"},{"id":"of-shipping-zipcode","setting":false,"placeholder":"Postal Code"}]},{"id":"credit-card-wrapper","visible":true,"label":{"id":"of-ccard-title","visible":true},"fields":[{"id":"of-ccard-number","setting":false,"placeholder":"Credit Card Number"},{"id":"of-ccard-cvc","setting":false,"placeholder":"CVC"}]},{"id":"profit-bump-wrapper","visible":true,"otoBgColor":"rgba(219,229,239,1)","otoBorderColor":"rgba(38,71,102,1)","otoTitleBgColor":"rgba(45,78,108,1)","otoArrowsColor":"rgba(255,177,58,1)","fields":[]},{"id":"order-summary-wrapper","visible":true,"orderDynamicBgColor":"rgba(242,242,242,1)","orderDynamicTexColor":"rgba(51,51,51,1)","fields":[]}]},"optin_type":{"showLabels":0,"fields":[{"name":"first_name","label":"Full Name","placeholder":"Enter Your Full Name","icon":"fa-user","required":1,"visible":1,"system":1,"additional":{}},{"name":"last_name","label":"Full Name","placeholder":"Enter Your Full Name","icon":"fa-user","required":1,"visible":1,"system":1,"additional":{}},{"name":"email","label":"Email","placeholder":"Enter Your Email","icon":"fa-envelope","required":1,"visible":1,"system":1,"additional":{}},{"name":"mobile_phone","label":"Mobile Phone","placeholder":"Enter Your Mobile Phone","icon":"fa-mobile","required":0,"visible":0,"system":1,"additional":{"sms_permission":0}},{"name":"fields_labels","label":"","placeholder":"","icon":"","required":0,"visible":1,"system":1,"additional":{}},{"name":"captcha","label":"Captcha","placeholder":"","icon":"","required":0,"visible":0,"system":1,"additional":{}},{"name":"gdpr_optin_approval","label":"SSBBY2NlcHQgVG8gUmVjZWl2ZSBBZGRpdGlvbmFsIEluZm8=","placeholder":"","icon":"fa-mobile","required":0,"visible":1,"system":1,"additional":{"gdpr_optin_approval":"1","sms_permission":0}}],"customFields":[],"sortedFields":[{"name":"first_name","label":"Full Name","placeholder":"Enter Your Full Name","icon":"fa-user","required":1,"visible":1,"system":1,"additional":{}},{"name":"first_name","label":"Full Name","placeholder":"Enter Your Full Name","icon":"fa-user","required":1,"visible":1,"system":1,"additional":{}},{"name":"last_name","label":"Full Name","placeholder":"Enter Your Full Name","icon":"fa-user","required":1,"visible":1,"system":1,"additional":{}},{"name":"email","label":"Email","placeholder":"Enter Your Email","icon":"fa-envelope","required":1,"visible":1,"system":1,"additional":{}},{"name":"mobile_phone","label":"Mobile Phone","placeholder":"Enter Your Mobile Phone","icon":"fa-mobile","required":0,"visible":0,"system":1,"additional":{"sms_permission":0}},{"name":"captcha","label":"Captcha","placeholder":"","icon":"","required":0,"visible":0,"system":1,"additional":{}}],"design":{"form_background_color":"rgb(245, 245, 245)","field_stroke":{"size":"1","color":"rgb(220, 220, 220)"},"field_icons":1,"button_color":"rgb(255, 158, 0)","button_stroke":{"size":"0","color":"rgba(255, 255, 255, 0.2)"},"button_box_shadow_color":"rgb(213, 139, 18) 0px 2px 0px 0px","field_size":"small","label_size":"16","label_color":"rgb(3, 3, 3)","input_color":"rgb(52, 152, 219)","control_text_color":"rgb(3, 3, 3)","control_text_size":"15"},"mappedFields":[]},"redirect_type":{"url":"https://112785.funnelpages.com/contact-us","target":1},"next_step":{"value":"5ecea1dde7bd0"},"click_to_email":{"value":""},"click_to_call":{"value":""},"jump_to_block":{},"content":{"header_text":"PHNwYW4gc3R5bGU9ImZvbnQtc2l6ZToyNHB4OyBmb250LWZhbWlseTonb3BlbiBzYW5zJzsiPjxzcGFuIHN0eWxlPSJsaW5lLWhlaWdodDoxLjRlbTsiPldlIEFyZSBFeGNpdGVkITwvc3Bhbj48L3NwYW4+","content_text":"PHNwYW4gc3R5bGU9ImZvbnQtc2l6ZTo0OHB4OyBmb250LWZhbWlseTonb3BlbiBzYW5zJzsiPjxzcGFuIHN0eWxlPSJsaW5lLWhlaWdodDowLjllbTsiPjxzdHJvbmc+UExFQVNFIEZJTEwgT1VUIFlPVVIgSU5GTyAgQkVMT1cgVE8gU1VCU0NSSUJFPC9zdHJvbmc+PC9zcGFuPjwvc3Bhbj4=","button_text":"dW5kZWZpbmVk","spam_text":"PHNwYW4gc3R5bGU9ImxpbmUtaGVpZ2h0OjEuMmVtOyI+V2UgaGF0ZSBTUEFNIGFuZCBwcm9taXNlIHRvIGtlZXAgeW91ciBlbWFpbCBhZGRyZXNzIHNhZmU8L3NwYW4+","sms_text":"UmVjZWl2ZSBTTVMgVGV4dCBVcGRhdGVzIC0gPHNwYW4+b3B0aW9uYWw8L3NwYW4+","sms_text2":"SSBBY2NlcHQgVG8gUmVjZWl2ZSBBZGRpdGlvbmFsIEluZm8="},"email_confirmation":{"enable":1,"subject":"V2UgQXJlIEV4Y2l0ZWQhIFlvdXIgSW4h","message":""},"integrations":{"name":"Form Optin Conversion","tag_id":""},"automation_enable":0,"thank_you":{"type":"popup","redirect_url":"","popup_options":{"background_color":"#ffffff","headline_visible":1,"icon_visible":1,"icon_url":"//my.funnelpages.com/assets-pb/images/thankyou-popup-icon.png","subheadline_visible":1,"button_visible":1,"button_color":"#ffa800","headline_text":"PHNwYW4gc3R5bGU9ImxpbmUtaGVpZ2h0OjEuNGVtOyI+VGhhbmsgWW91IEZvciBDb250YWN0aW5nIFVzPC9zcGFuPg==","subeadline_text":"PHNwYW4gc3R5bGU9ImxpbmUtaGVpZ2h0OjEuNGVtOyI+UGxlYXNlIENoZWNrIFlvdXIgRW1haWw8YnIgLz5XZSBXaWxsIEJlIEZvbGxvd2luZyBVcCBTaG9ydGx5PC9zcGFuPg==","button_text":"Q2xvc2U="}}}

Innocent spouses face more serious problems than injured spouses. When you complete a tax return, you sign your return with penalties under perjury. Even if you were unaware of your spouse’s understatement, the IRS counts this misrepresentation as tax fraud and imposes serious consequences for it.

Legally, if the IRS suspects fraud in your joint return, it can:

- Audit You

An IRS Audit is an extensive review of your taxes and financial records to ensure you reported everything correctly. Undergoing an audit is a time-intensive and costly process. It demands years of documentation and, at times, even in-person interviews. Most people need to hire a professional to represent them during an audit.

- Impose Penalties and Fees

Even if you file on time, you may still be charged a late payment penalty if your spouse under reported their income and the IRS finds out. They can also charge interest on the underpayment as well. The IRS can charge steep fines for fraud, up to $250,000.

- Make Criminal Charges

Besides potentially owing thousands of dollars, the IRS can make criminal charges for tax fraud, a felony punishable by up to five years in prison. If you’re investigated, the chances of getting arrested are pretty small—less than 20 percent—but approximately 3,000 people per year are convicted for tax fraud.

For relief of liability from the above penalties, you can file an innocent spouse claim. The innocent spouse rule stipulates that you must have signed and filed a joint return without full knowledge of your spouse’s true financial situation. Married persons who did not file joint returns, but live in community property states, may also qualify for innocent spouse relief.

For relief of liability from the above penalties, you can file an innocent spouse claim. The innocent spouse rule stipulates that you must have signed and filed a joint return without full knowledge of your spouse’s true financial situation. Married persons who did not file joint returns, but live in community property states, may also qualify for innocent spouse relief.

Claims for Injured Spouse vs Innocent Spouse

If you’re seeking innocent spouse relief, you need to first file Form 8857 separately from your tax return. The IRS will evaluate the information you provide on your innocent spouse claim, along with any supporting documentation, to determine if you qualify. After receiving Form 8857, they will contact your spouse and invite them in on the process. There is no exception for this, even in cases of spousal abuse. You should file your innocent spouse claim as soon as you become aware of a tax liability for which you believe only your spouse or former spouse should be held responsible. Bear in mind that you can only invoke the innocent spouse rule up to two years after the incorrect return was filed.

For injured spouse claim, you need to submit Form 8379, Injured Spouse Allocation. Essentially, this form asks the IRS to pay attention to which member of the couple has a refund and which has the debt. You can submit Form 8357 alongside your joint tax return, or file it separately after receiving your Notice of Offset. If you file an injured spouse claim included in your tax return, the IRS will process your request for allocation prior to offsetting funds. You can make an injured spouse claim electronically or by paper. When you file a paper return, include Form 8379 and write “INJURED SPOUSE” on the top left corner of your Form 1040, 1040-A, or 1040-EZ. For circumstances in which you were unaware of your spouse’s past debts and seek injured spouse relief after your refund was seized, be sure to include both you and your spouse’s Social Security number as it appeared on the return in the paperwork. Only you, the injured spouse, needs to sign the injured spouse claim.

If you are seeking help as an injured or innocent spouse, allow the trusted professionals at US Tax Relief to walk you through the claims process. We can assist by helping you save you time, money, and stress.

For injured spouse claim, you need to submit Form 8379, Injured Spouse Allocation. Essentially, this form asks the IRS to pay attention to which member of the couple has a refund and which has the debt. You can submit Form 8357 alongside your joint tax return, or file it separately after receiving your Notice of Offset. If you file an injured spouse claim included in your tax return, the IRS will process your request for allocation prior to offsetting funds. You can make an injured spouse claim electronically or by paper. When you file a paper return, include Form 8379 and write “INJURED SPOUSE” on the top left corner of your Form 1040, 1040-A, or 1040-EZ. For circumstances in which you were unaware of your spouse’s past debts and seek injured spouse relief after your refund was seized, be sure to include both you and your spouse’s Social Security number as it appeared on the return in the paperwork. Only you, the injured spouse, needs to sign the injured spouse claim.

If you are seeking help as an injured or innocent spouse, allow the trusted professionals at US Tax Relief to walk you through the claims process. We can assist by helping you save you time, money, and stress.

Speak With One Of Our Tax Professionals Today!

SUBMIT

{"name":"US Tax Relief Form","action_type":"3","optin_action_type":"5","form_redirect_type":"3","form_redirect_funnel_url":"next-funnel","form_redirect_custom_url":"","order_form_settings":{"containers":[{"id":"personal-info-wrapper","visible":true,"label":{"id":"of-personal-title","visible":true},"fields":[{"id":"of-full-name","setting":false,"placeholder":"Full Name"},{"id":"of-field-email","setting":false,"placeholder":"Email Address"},{"id":"of-phone-number","setting":true,"visible":false,"require":true,"placeholder":"Enter Your Mobile Phone","additional":{"sms_permission":0}},{"id":"of-gdpr-optin-approval","label":"I Accept To Receive Additional Info","placeholder":"","icon":"fa-mobile","required":0,"visible":0,"system":1,"additional":{"gdpr_optin_approval":"1"}}]},{"id":"shipping-information-wrapper","visible":false,"label":{"id":"of-shipping-title","visible":true},"fields":[{"id":"of-shipping-address","setting":false,"placeholder":"Address"},{"id":"of-shipping-city","setting":false,"placeholder":"City"},{"id":"of-shipping-state","setting":false,"placeholder":"State"},{"id":"of-shipping-zipcode","setting":false,"placeholder":"Postal Code"}]},{"id":"credit-card-wrapper","visible":true,"label":{"id":"of-ccard-title","visible":true},"fields":[{"id":"of-ccard-number","setting":false,"placeholder":"Credit Card Number"},{"id":"of-ccard-cvc","setting":false,"placeholder":"CVC"}]},{"id":"profit-bump-wrapper","visible":true,"otoBgColor":"rgba(219,229,239,1)","otoBorderColor":"rgba(38,71,102,1)","otoTitleBgColor":"rgba(45,78,108,1)","otoArrowsColor":"rgba(255,177,58,1)","fields":[]},{"id":"order-summary-wrapper","visible":true,"orderDynamicBgColor":"rgba(242,242,242,1)","orderDynamicTexColor":"rgba(51,51,51,1)","fields":[]}]},"optin_type":{"showLabels":0,"fields":[{"name":"first_name","label":"First Name","placeholder":"Enter Your Full Name","icon":"fa-user","required":1,"visible":1,"system":1,"additional":{}},{"name":"last_name","label":"First Name","placeholder":"Enter Your Full Name","icon":"fa-user","required":1,"visible":1,"system":1,"additional":{}},{"name":"email","label":"Email","placeholder":"Enter Your Email","icon":"fa-envelope","required":1,"visible":1,"system":1,"additional":{}},{"name":"mobile_phone","label":"Mobile Phone","placeholder":"Enter Your Mobile Phone","icon":"fa-mobile","required":0,"visible":0,"system":1,"additional":{"sms_permission":0}},{"name":"fields_labels","label":"","placeholder":"","icon":"","required":0,"visible":1,"system":1,"additional":{}},{"name":"captcha","label":"Captcha","placeholder":"","icon":"","required":0,"visible":0,"system":1,"additional":{}},{"name":"gdpr_optin_approval","label":"SSBBY2NlcHQgVG8gUmVjZWl2ZSBBZGRpdGlvbmFsIEluZm8=","placeholder":"","icon":"fa-mobile","required":0,"visible":1,"system":1,"additional":{"gdpr_optin_approval":"2","sms_permission":0}}],"customFields":[],"sortedFields":[{"name":"first_name","label":"First Name","placeholder":"Enter Your Full Name","icon":"fa-user","required":1,"visible":1,"system":1,"additional":{}},{"name":"email","label":"Email","placeholder":"Enter Your Email","icon":"fa-envelope","required":1,"visible":1,"system":1,"additional":{}},{"name":"mobile_phone","label":"Mobile Phone","placeholder":"Enter Your Mobile Phone","icon":"fa-mobile","required":0,"visible":0,"system":1,"additional":{"sms_permission":0}},{"name":"captcha","label":"Captcha","placeholder":"","icon":"","required":0,"visible":0,"system":1,"additional":{}}],"design":{"form_background_color":"rgb(245, 245, 245)","field_stroke":{"size":"1","color":"rgb(220, 220, 220)"},"field_icons":0,"button_color":"rgb(255, 158, 0)","button_stroke":{"size":"0","color":"rgba(255, 255, 255, 0.2)"},"button_box_shadow_color":"rgb(213, 139, 18) 0px 2px 0px 0px","field_size":"small","label_size":"16","label_color":"rgba(255,255,255,0)","input_color":"rgb(52, 152, 219)","control_text_color":"rgb(0, 0, 0)","control_text_size":"16"},"mappedFields":[]},"redirect_type":{"url":"","target":0},"next_step":{"value":"next-funnel"},"click_to_email":{"value":""},"click_to_call":{"value":""},"jump_to_block":{},"content":{"header_text":"PHNwYW4gc3R5bGU9ImZvbnQtc2l6ZToyNHB4OyBmb250LWZhbWlseTonb3BlbiBzYW5zJzsiPjxzcGFuIHN0eWxlPSJsaW5lLWhlaWdodDoxLjRlbTsiPldlIEFyZSBFeGNpdGVkITwvc3Bhbj48L3NwYW4+","content_text":"PHNwYW4gc3R5bGU9ImZvbnQtc2l6ZTo0OHB4OyBmb250LWZhbWlseTonb3BlbiBzYW5zJzsiPjxzcGFuIHN0eWxlPSJsaW5lLWhlaWdodDowLjllbTsiPjxzdHJvbmc+UExFQVNFIEZJTEwgT1VUIFlPVVIgSU5GT0JFTE9XIFRPIFNVQlNDUklCRTwvc3Ryb25nPjwvc3Bhbj48L3NwYW4+","button_text":"PHNwYW4gc3R5bGU9ImZvbnQtc2l6ZToyN3B4OyBmb250LWZhbWlseTonb3BlbiBzYW5zJzsiPjxzcGFuIHN0eWxlPSJsaW5lLWhlaWdodDoxZW07Ij48c3Ryb25nPlNFQ1VSRSBNWSBTUE9UPC9zdHJvbmc+IDwvc3Bhbj4gPC9zcGFuPg==","spam_text":"PHNwYW4gc3R5bGU9ImxpbmUtaGVpZ2h0OjEuMmVtOyI+V2UgaGF0ZSBTUEFNIGFuZCBwcm9taXNlIHRvIGtlZXAgeW91ciBlbWFpbCBhZGRyZXNzIHNhZmU8L3NwYW4+","sms_text":"UmVjZWl2ZSBTTVMgVGV4dCBVcGRhdGVzIC0gPHNwYW4+b3B0aW9uYWw8L3NwYW4+","sms_text2":"SSBBY2NlcHQgVG8gUmVjZWl2ZSBBZGRpdGlvbmFsIEluZm8="},"email_confirmation":{"enable":1,"subject":"VVMgVGF4IFJlbGllZg==","message":"T24gb2Ygb3VyIHRheCBwcm9mZXNzaW9uYWxzIHdpbGwgYmUgY29udGFjdGluZyB5b3UsIHVzdWFsbHkgd2l0aGluIDI0IGhvdXJzLjxiciAvPgo8YnIgLz4KVGhhbmsgeW91ITxiciAvPgo8YnIgLz4KVVMgVGF4IFJlbGllZiBUZWFtPGJyIC8+Cjg3Ny00MjAtMjM0MTxiciAvPgombmJzcDs="},"integrations":{"name":"US Tax Relief Form","tag_id":""},"automation_enable":0,"thank_you":{"type":"popup","redirect_url":"","popup_options":{"background_color":"#ffffff","headline_visible":1,"icon_visible":1,"icon_url":"//my.funnelpages.com/assets-pb/images/thankyou-popup-icon.png","subheadline_visible":1,"button_visible":1,"button_color":"#ffa800","headline_text":"PHNwYW4gc3R5bGU9ImxpbmUtaGVpZ2h0OjEuNGVtOyI+VGhhbmsgWW91IEZvciBDb250YWN0aW5nIFVzPC9zcGFuPg==","subeadline_text":"PHNwYW4gc3R5bGU9ImxpbmUtaGVpZ2h0OjEuNGVtOyI+UGxlYXNlIENoZWNrIFlvdXIgRW1haWw8YnIgLz5XZSBXaWxsIEJlIEZvbGxvd2luZyBVcCBTaG9ydGx5PC9zcGFuPg==","button_text":"Q2xvc2U="}}}

Removed Automation Delay

Added Automation Delay

No Active Automations

MYBRANDINGLOGO

Phone: (877) 420-2341

Hours: 8:00AM to 5:30PM

Monday through Friday

US Tax Relief Agency

732- Eden Way North, Suite 250

Chesapeake, VA 23320

© 2021 US Tax Relief Agency All Rights Reserved. 732-E Eden Way North, Suite 250, , Chesapeake, VA 23320 . Contact Us . Terms of Service . Privacy Policy